Financing Long-term Care In the US: An Overview

The current system doesn't work.

This is the first of a series on financing long-term care in the US. In part one, we provide a brief overview of the long-term care landscape and the critical financing issues that the US faces. Part two can be found here. We also review how other countries finance long-term care. In later posts, we will examine the implications of various proposed funding options. We obviously have a preference: use health savings accounts (HSAs) to finance long-term care and we will explain why this is the best option.

At least 60% of Americans will need some form of long-term care (LTC) in their lives. In fact, half of Americans who are aged 65 years now will need LTC at some point in the future. LTC is a catch-all term for care for people who need some help — healthcare, personal care, and social support — continuously to perform routine daily activities. An aging population increases the needs for LTC, but the elderly are not alone. Other care recipients include patients who need post-acute care and those suffering from mental illness who may have lost or never acquired functional independence. Long-term care occurs within different settings — at home, nursing home, skilled nursing home, community day care — for delivery of what are usually referred to as Long-Term Services and Support (LTSS). It is important to reiterate that LTC is not only medical care.

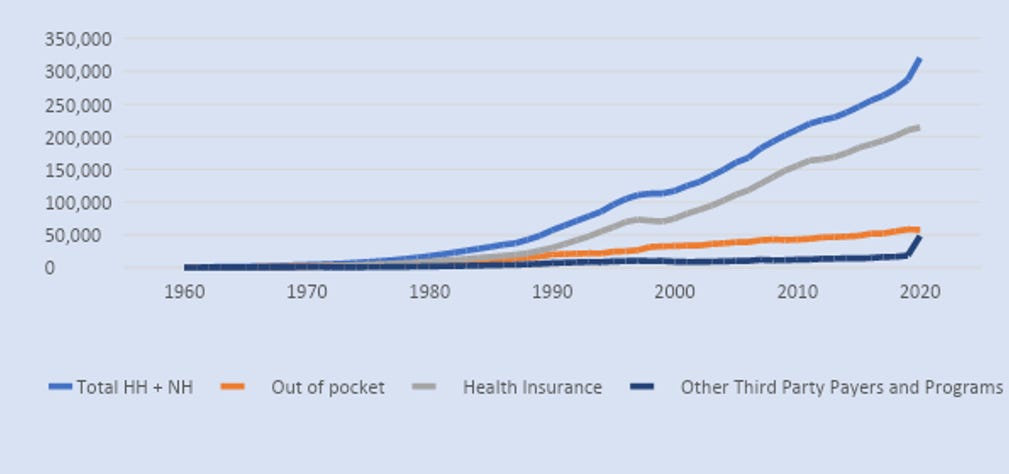

The average person will need about two years of community-based LTSS at some point, and among those who do, almost two-thirds would be in transition nursing homes, where another half would stay for a year. About a fifth of all nursing home residents stay for up to five years. In 2015, the government reported that the average person would need about $135,000 to finance LTSS. But costs vary depending on care needs, sex, state of residence, and other factors, and most Americans struggle to pay for it. For example, the lifetime long-term care cost for someone diagnosed with dementia is more than $320,000. It’s not uncommon to hear families lament the costs — monetary, foregone labor hours, and mental stress — of caring for the elderly. The most expensive support service is care in nursing homes, especially for those with common mental illnesses such as dementia. However, most of the LTSS needed is provided by family caregivers. Estimates vary but according to the AARP, in 2017, the value of unpaid family services was $470 billion, almost the same as compensated care. Figure 1 below shows the total spending on LTSS from all sources. Most of LTSS is financed through insurance (Medicaid, Medicare, and private insurance).

Financing Options for LTC

LTSS in the US has been financed through a mix of out-of-pocket, private insurance, and public insurance (Medicare and Medicaid) sources. Medicaid is by far the largest payer of LTSS. In 2020, only 5.4% of Medicaid beneficiaries received LTSS, yet they accounted for nearly a third of all Medicaid expenditures. In 2020, Americans spent $470 billion on LTSS, 70% of which was funded by public insurance (Medicaid 42%, Medicare 18%, and others). Private funds, including insurance, only account for 27%. As Figure 2 below, reproduced from CMS, shows, the share of Medicaid expenditures going to LTSS has been on a downward trend since 1988 but has seen an upswing in recent years.

As is common with healthcare in the US, out-of-pocket spending has been decreasing. For example, in 2020, 23% of nursing home stays, which is just one part of LTSS, was financed out of pocket, compared with 59% by insurance.

The private insurance market for financing LTC has practically collapsed. In the year 2000, 125 insurers offered long-term care policies. By 2016, there were only 17. The steep drop is because insurers mispriced policies, making those products unprofitable. It is still possible to get coverage, but it is expensive. For example, a $165,000 coverage would cost the average 55-year-old male $950 per year, rising to $2,500 by age 65. About 30% of applicants are denied coverage and the average policy is issued at age 51. The truth is that financing LTC via private insurance is complicated and unavailable to most Americans. These challenges with LTC insurance (LTCI) have led many politicians to offer public insurance proposals. In fact, Washington state has a mandatory public LTCI. Effective January 1, 2023, residents there will pay a payroll tax of 0.58% to obtain LTCI coverage but can opt out only if they buy private LTCI. Similar policies are in place in Germany and Japan.

For those who qualify, Medicaid is the payer of last resort particularly for institutional long-term care such as nursing homes or skilled nursing facilities. Subject to various state rules, beneficiaries who exceed income limits must transfer their assets to Medicaid or contribute to the cost of care. By law, the estates of Medicaid LTC beneficiaries must reimburse Medicaid for the cost of care through the Asset Recovery Program after their death. Estimates of recovered assets are few, but the most recent estimate comes from Medicaid and CHIP Payment Access Commission (MACPAC), showing that in 2019, states recovered $733 million from beneficiary estates, representing about 0.62% of LTSS. In 2004, the percentage of Medicaid nursing home spending recovered was 0.78% ($361 million from estates). Given the low amounts recovered from estates, it is perhaps time to repeal the law and allow Medicaid LTC beneficiaries to pass on assets to their heirs. In addition, the rule disproportionately affects those with small estates.

There have been several efforts to understand the failures of the LTCI market, including most recently a task force convened by the Department of the Treasury. Their recommendations included offering tax incentives, financial literacy and education, regulatory reform, and innovation. Politicians from across the political spectrum have tried to promote insurance as the main financing mechanism. Democrats are generally in favor of public insurance options while Republicans propose to allow for tax-exempt distributions from retirement funds to pay for LTCI. We don’t believe that using pre-retirement 401k distributions to pay for LTCI premiums is a good idea. Like student loans, insurers could just price to the maximum penalty-free distribution allowed. An insurance product that is very likely to be used will be expensive. If you live in a flood prone area, flood insurance will be expensive or the insurance companies will leave the market eventually.

The truth is LTC places undue financial and mental strain on all Americans — the elderly and their families, local communities, and state and federal governments. As we’ve established, not all long-term care is medical care. It’s almost like an oil change for your car — you are more likely to need it than not, and therefore we must plan for it. Unfortunately, that stage coincides with our least productive years. But just as we save for kids’ college or save for down payments for a house, we can combine personal savings, public financing and private insurance to finance an inevitable expense in a way that does not place undue stress on all involved. Of course, saving for a home or vehicle maintenance is very different from saving for LTC. However, the young need to be encouraged to start thinking and planning for LTC, perhaps at the same time that they are introduced to retirement savings such as 401k.

In part two of this post, we propose that rules governing HSAs be amended to allow Americans to save for their long-term care needs. We discuss how HSAs can be combined with other arrangements, including informal family care, to reduce the burden on families.