Long-Term Care Financing: A Tour Around the World

Is there a "best" financing model out there?

There is remarkable variation in how countries finance long-term care (LTC).

Public and social insurance systems dominate most OECD countries.

France has a uniquely robust private long-term care insurance system that the US could learn from.

Ultimately, the US would benefit from a mix of funding mechanisms that meet the needs of various populations.

This is the third in a series of posts that examine long-term care in the United States. Previously, we provided an overview of the financing challenges in the US followed by a proposal to encourage young Americans to plan and save for future long-term care expenses through tax-advantaged plans. Today’s post takes a quick tour around the world to examine how a select group of countries finance long-term care support services (LTSS). This post draws from voluminous reports from the OECD, the European Union, and many others. We look at financing LTSS in mainly OECD countries, including Canada, Germany, France, Japan, the Netherlands, and the United Kingdom. We also examine non-OECD countries with unique funding mechanisms such as Singapore. We would like to thank Howard Gleckman for giving us some pointers.

This is a long post but scroll to the bottom for a table that summarizes the key features of LTC financing in the countries discussed here. We examine the funding mechanisms through 1) the national philosophy regarding paying for medical care, 2) the expected relationship between children and their aged parents, and 3) the funding mix, including public or social insurance, and private insurance. We also review how much each country spends on providing LTSS in terms of GDP.

National Funding Approach

Societies vary widely in how they think about paying for care and the role of children in caring for aging parents. In countries such as Singapore, there is a shared underlying presumption that individuals are responsible for their own health and must therefore contribute to the cost of their medical care. In the Nordic countries, healthcare — and by extension long-term care — is deemed the responsibility of society, and therefore the state and other agencies of government often provide generous and comprehensive benefits to cover LTSS needs. These benefits are funded through general taxes. Australia has a funding approach similar to the Nordic countries, whereby LTSS is almost fully funded by the government. In addition, these countries place different levels of emphasis on the role of families in providing LTSS. Again, in Singapore and most Asian countries, families are assumed to be primarily responsible for taking care of the elderly. In Singapore, for example, out-of-pocket costs comprise 40% of all LTSS funding while the government is only responsible for 42%. About two-thirds of all LTSS are provided by voluntary non-governmental welfare organizations, again relying on the presumption that the family is the primary caregiver.

Other countries enforce personal responsibility through mandated insurance. Prominent among them are Germany, Japan, and South Korea.

National Spending

According to the most recent data, among the countries we studied, Singapore spends the lowest share of GDP on LTSS: 0.9% in 2016, compared to the US (1.6%), Canada and Japan (2%), Germany (2.2%), France (2.4%), Sweden (3.4%), and the Netherlands (4.1%).

Social Insurance

The social insurance model is a common funding mechanism for LTSS. Residents typically contribute to a national fund, which is used to pay for LTSS. There are significant variations to these models, which sometimes include mandatory participation and means-tested benefits. Funding sources vary, from payroll taxes (Germany) to local/municipal taxes (Sweden). In Germany, the tax rate is progressive, based on household income, and access to benefits is based on need of care (five levels). Some researchers have estimated that, across the world, a third of LTSS funding is via social insurance/security systems, typically a pay-as-you-go model where current taxes fund current benefits of the aged. Other countries that use the social insurance model include Japan, where participation has been mandatory since 2000. Funding is evenly split between insurance premiums and general taxes. As of 2015, individuals above a certain income level have a co-payment of 20% for benefits.

In South Korea, LTC insurance was introduced in 2008 and a portion of individuals’ health insurance premiums are automatically allocated to LTC insurance (LTCI). On average, almost a third of LTSS is funded by insurance. Tax subsidies comprise a fifth of all LTSS spending. Individuals often make co-payments ranging from 15-20%. Singapore uses its ElderShield program to fund LTSS. Individuals who enroll in the optional MediSave program are automatically enrolled in the ElderShield program when they turn 40 years old, although they can opt out. They are then randomly assigned to one of three insurance companies. Premiums are individually rated, meaning they vary with age or gender. Voluntary organizations receive subsidies from the government to provide LTSS. Singapore deserves its own post!

Private Insurance

Funding LTSS via private insurance is still very uncommon across the world and in our list of countries. The share of LTSS financed by LTCI is largest in the US followed by Japan and France. As we note below, the French market for LTCI is actually more robust than that of the US due to the steeply means-tested US/French public LTC benefits program.

Universal Benefits

This class of financing includes universal benefits available to eligible individuals, whether in cash or through the provision of services. Australia is perhaps the best example of universal benefits. All individuals who are eligible receive LTSS through highly regulated service providers. Sweden also uses this approach. In both countries, benefits are administered by local municipalities, but funding sources differ. LTC is highly decentralized in Sweden as opposed to Australia, and municipalities regulate eligibility and levels of service. Municipalities also provide minimal cash benefits (about 3% of the total value of care) to some qualified family caregivers. Recently, there has been some movement toward a more-market friendly approach, where private providers deliver publicly funded care, like Australia and England. For countries that provide universal benefits, funding is generally from tax revenues, though there may be some private contributions as in England. At 2.9% of GDP, LTSS spending in Sweden is among the highest in Europe, second only to the Netherlands, which, as we see below, offered very generous benefits in institutional settings prior to major 2013 reforms.

Because of the UK’s devolved NHS system, England, Scotland and Wales each have very different systems. In Scotland, provision of LTC is universal and free, while in England, individuals are largely responsible for their LTC needs, though there is considerable public support through local councils. In Wales and England, long-term care or social care is heavily means-tested, with public support only available to the neediest. Once individuals meet the eligibility criteria, however, care is fully funded by the local authority. New Zealand similarly provides means-tested comprehensive LTSS. These are publicly funded. Similar to Medicaid in the US, beneficiaries must spend down their assets before receiving public funds. Those above the income threshold pay for their care up to a maximum amount.

Country Focus

Funding mechanisms for LTSS vary widely as we’ve observed. We are particularly interested in Canada, Australia, France, and the Netherlands, which have very different funding schemes.

Canada

Healthcare in Canada is fascinating, not because it is state funded, but because much of the funding and implementation decisions are left to provinces. This is also the case for long-term care. There is no national LTC program but rather various programs by provinces to take care of the disabled and elderly. As a result, funding mechanisms and benefits vary widely across the provinces and territories. In general, informal care comprises between 66% and 84% of all LTSS in Canada. In Ontario, the most populous province, long-term care is covered under its healthcare system, with the public health insurance being responsible for 70% of all LTSS funding. Private insurance and out-of-pocket expenses make up 22% of LTSS funding.

Australia

Funding of LTSS in Australia is primarily provided by the local, state and federal governments, though some individuals make co-payments. Access to care is universal and available to all who need it. Care is delivered through several programs, each tailored to meet specific needs, including the home support program (CHSP), the home care packages (HCP) program, residential aged care, and flexible care. CHSP is similar to the Home and Community-Based Services (HCBS) in the US, where individuals are encouraged to age at home and receive support to do so. It is primarily aimed at those with the lowest level of support. HCP services are more intensive than CHSPs but also targeted to those who can age at home. Care needs are grouped into four levels, with level 4 (most severe) receiving the largest benefit amounts. The generosity of care means that there are often wait-lists. According to the government, about 75,000 people were on waiting lists to receive HCP services in 2019. Residential care is available to those who need more intensive care outside of their homes. Care is provided by private organizations reimbursed by the government. If they are able, beneficiaries are required to contribute toward their care. Individuals are typically responsible for their accommodation but the government pays for those who cannot afford it.

France

France has a uniquely private-public partnership arrangement to finance LTSS. While public benefits exist to cover assistance for people over age 60, these payments are steeply means-tested as well as dependent on severity (six levels) of any disability. Monthly benefits range from $760 for the least severe level of dependency to $1,770 for the most severe level. Beneficiaries are free to spend on resources needed for their care. These means-tested amounts are grossly insufficient to cover expenses, so most French buy private supplemental LTCI, often through their employers. Due to the significantly higher uptake of private LTCI, premiums are significantly lower than in the US. In 2010, for example, the average monthly premium for LTCI in the US was $2,283 compared to $469 in France (subject to the usual purchasing power parity caveats). Similar to employer-sponsored health insurance in the US, French employers sponsor LTCI for their employees with premiums that are significantly lower than that of the non-employer private markets. Employee contributions are converted into annuities upon retirement and, even more importantly, they do not need to make any more monthly premiums to receive payouts when needed.

Perhaps there are some lessons here for the US. While the private LTCI market in the US has largely stalled or collapsed for private individuals, federal employees have the option of enrolling in an LTCI plan.

Netherlands

Financing LTC in the Netherlands offers a serious lesson in public financing. By 1997, the universal public long-term care insurance scheme covered nursing home and institutional care, home health, ambulatory mental health, social assistance, and residential care for the elderly. As a result, most long-term care happens in institutional settings. Reforms were implemented in 2013, when admission to institutional care was limited to only the most severe levels of impairment (eight levels of impairment). In 2015, municipalities assumed responsibility for some aspects of care including home care, which was funded through block grants from the central government. The block grants encouraged municipalities to find ways of saving money. Co-payments from beneficiaries comprise about 9% of LTSS spending.

Conclusion

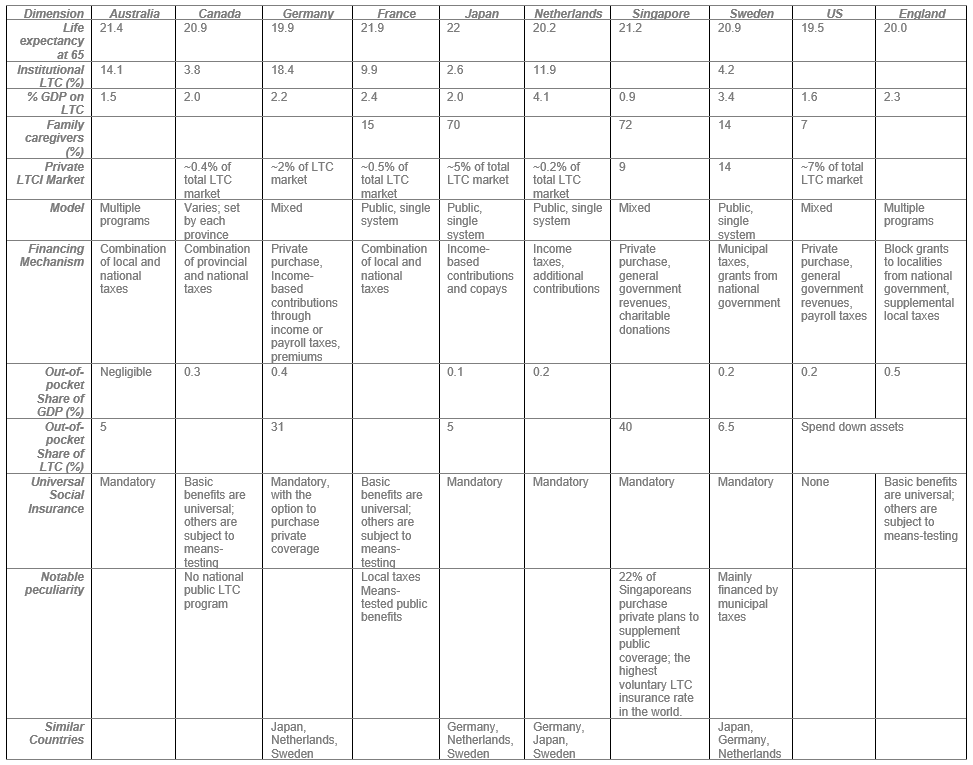

There are a lot more countries that we reviewed, but we can’t reasonably summarize our findings in a single post. The table below provides a quick summary of the key features of the LTSS funding mechanisms in a selection of countries.

This tour could easily fill hundreds of pages, but we wanted to highlight a select few that show the breadth of options. Countries develop funding mechanisms based on some underlying shared view of the role of individuals, families and society at large. We are not sure we found the “best model” through this tour. How do we define best? Quality of outcomes, cost-effectiveness, coverage, or individual responsibility? Perhaps a combination of funding mechanisms needs to be considered. Whether French policymakers intended it or not, it is interesting that they managed to create a somewhat robust private LTCI market. Singapore is also unique in its use of private-public partnership to provide LTSS.